09 Jul Carve-Out Valuations: Carving Through Layers of SBA Deals

Written by: Matthew Safft, CVA & Todd Kutcher, CVA

(5 – 7 minute read)

Many businesses offer multiple products and services to diversify the generation of revenues. In some instances, certain product/service lines or divisions of a business can be sold on an open market separate from the entity. Additionally, certain business owners also operate multiple locations of the same business type within a single entity (i.e. restaurants, retail stores, franchises, etc.). However, when analyzing these segments of businesses or separate locations (commonly referred to as a carve-out), there are several additional considerations to be made during the analytical process.

A common concern amongst buyers, sellers, lenders, and appraisers when analyzing a segment of a business pertains to the quality and reliability of the financial statements available. When assessing a sophisticated practice, financial statements may be readily available by division or location, which would reconcile to the consolidated financial statements. However, these statements rarely exist in smaller, closely held businesses. Therefore, the following steps should be taken during the early stages of analysis:

- Determine what is being sold

- Determine the financial statements that are obtainable

- Determine whether there is sufficient information to proceed with the proposed transaction

Step 1: Determine What is Being Sold

Although this consideration seems simple in nature, it can sometimes be difficult for a lender, buyer, or appraiser to obtain enough information to accurately determine the line(s) of business or location(s) transferring in a proposed transaction. In the most ideal cases, the portion of the business being sold can be clearly identified. A simple example would be a restaurant with an independent catering service. If the catering services do not depend on the restaurant for operations, operate under separate trade names, and operate from separate locations, then any party involved should be able to distinguish the two divisions if a single division were to be sold. Another example would be a FedEx service contractor that intends to sell a specific route from a portfolio of owned routes. In this instance, the routes being sold should be clearly segmented from the remaining operations.

On the contrary, certain lines of business cannot be distinguished due to several factors. If all divisions of the consolidated operation operate from the same location(s), operate under the same trade name, or depend on the staff or processes, then it can be difficult to distinguish the cost structure of each division individually. A common example is an e-commerce business that sells many (unrelated) products and services under the same trade name but depends on the same warehouse and personnel to sustain operations. In these scenarios, it may be unreasonable to assume that both lines of business can operate independently with no further considerations. For these transactions, all parties involved should be aware of the specific facts, circumstances, and post-closing actions to be taken to separate the consolidated operations.

Step 2: Determine the Financial Statements that are Obtainable

Once the subject of business has been clearly identified, all parties involved should determine the financial statements that reflect the operations of the carved-out division. As with any transaction, the stronger the quality of the financial statements used in analysis, the more reliable the result. Therefore, it is highly advisable to have a qualified professional prepare the financial statements by division to minimize any risks regarding financial statement quality. Assuming financial statements by division are not prepared separately from the consolidated operations, a general ranking of financial statement quality for carved-out divisions, from highest to lowest quality, can be found below:

- Accountant Audited or Reviewed Financial Statements by Division or Location

- Management Prepared Statements that reconcile to consolidated operations

- Management Prepared Statements by division or location (reconciliation unavailable but each expense analyzed)

- Pro-rated Financial Statements (typically a % of revenue)

- Proof of Record of Sales and COGS

- Projections of carved-out operations (no financials available)

All parties should be aware of the risks of relying on internally (management) prepared statements, which could include a misstatement of revenues and expenses, fraudulent reporting of operations by division, or the oversight/omission of key operating expenses. If any party is relying on management prepared statements, they should be thoroughly examined in comparison to the consolidated operation to ensure the provided statements seem reasonable. Additionally, for SBA transactions, the Standard Operating Procedures (SOP 50 10 7.1 as of the date of this newsletter) state the following [as per page 72 of SOP 50 10 7.1]:

For a change of ownership, the SBA Lender must verify the seller’s business tax returns or a sole proprietor’s Schedule C. For 7(a) loans, when there is an acquisition of a division or a segment of an existing business, other forms of verification acceptable to SBA may be used in lieu of the IRS Form 4506-C or IRS Form 8821 (e.g. Sales tax payment records).

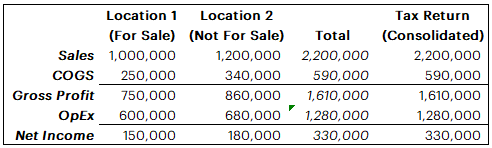

The following is an illustrative example of a reconciliation of a two-location restaurant to the federal tax returns:

As seen above, the total of revenues and expenses for both locations match the total reported revenue and expenses on the consolidated federal tax returns. If any amounts do not reconcile, then the provided financial statements by location may not be reliable for analysis, and the appropriate questions should be asked by an appraiser.

Step 3: Determine Whether There is Sufficient Information to Proceed with the Proposed Transaction

Once the first two steps have been completed, the final step is to make an educated decision as to whether there is enough information to proceed with the purchase or financing of the proposed division. Some questions to ask yourself are as follows:

- Am I confident that the segment(s) being purchased/financed can operate independently?

- Do I have sufficient information to determine the reasonability of the financial statements and assumptions provided?

- Have all questions and concerns regarding both the documents provided and the proposed transaction been adequately addressed?

The responses to the above questions are highly subjective in nature – personal/institutional risk tolerance, along with the availability and accessibility of information influence the final decision. Regardless, the overarching theme for each transaction remains constant: the proposed transaction should make sense to all parties involved. If insufficient information is available, then it is highly advisable to delay further consideration until the appropriate financial statements are available for an appraiser to analyze.

Analyzing a carve-out of a business is accompanied by many additional risks, which include the sustainability of post-closing operations, quality of financial statements, and more complicated financial statement analysis. When examining such deals, it is imperative to review all available documents to assess these factors in detail to arrive at the most prudent lending decision.